Key Highlights

- February PCE and March CPI data expected this week, marking initial inflation measurements following Iran conflict outbreak

- March employment figures exceeded forecasts with 178,000 new positions versus projected 65,000

- Crude prices surged more than 50% since conflict initiation, national gasoline averages surpassed $4 threshold

- Delta Air Lines earnings release scheduled for Wednesday, providing insight into aviation sector fuel cost pressures

- Major equity benchmarks concluded five consecutive weeks of declines, posting gains exceeding 3%

Investors are preparing for a pivotal trading week characterized by critical inflation metrics, quarterly corporate reports, and evolving Middle East conflict dynamics.

Equity markets posted gains last week, with the S&P 500 climbing 1.6%, the Dow Jones advancing 1.2%, and the Nasdaq rallying 2.2%. This performance snapped a five-week decline across all three benchmarks. Year-to-date, the S&P 500 and Dow remain negative, down 3.8% and 3.2%, respectively.

March employment data significantly outperformed projections on Friday. Nonfarm payroll additions totaled 178,000, substantially exceeding the consensus estimate of 65,000. This represented a sharp reversal from February’s 92,000 job contraction.

“The key message is equilibrium,” stated Gina Bolvin, president of Bolvin Wealth Management Group. “Robust employment growth diminishes immediate pressure for monetary easing, though it doesn’t alter the underlying deceleration pattern.”

Michael Feroli, JPMorgan Chase’s chief US economist, noted the data provided “somewhat greater assurance that economic expansion can absorb the current energy price disruption without substantial lasting harm.”

Critical Inflation Metrics on Horizon

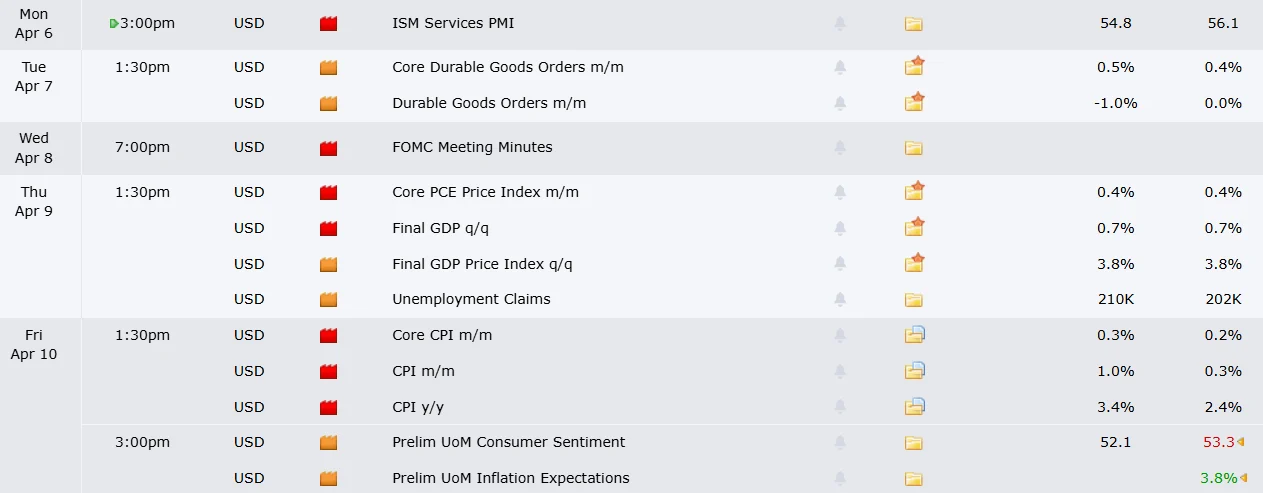

Thursday features the release of February’s Personal Consumption Expenditures index, a pivotal inflation gauge monitored extensively by Federal Reserve policymakers. Analyst consensus anticipates a 0.4% monthly increase and 2.8% annual growth.

The week’s most significant release arrives Friday with March’s Consumer Price Index. Economic forecasters project a 0.9% monthly advance and 3.4% yearly increase. February’s CPI registered at 2.4% annually. This upcoming report represents the initial measurement incorporating Iran conflict effects on consumer prices.

National average gasoline prices exceeded $4 per gallon last week, based on AAA data. Goldman Sachs analyst Ben Shumway observed that escalating prices are “contributing to additional declines in consumer sentiment from existing depressed thresholds.”

Andy Schneider, senior US economist at BNP Paribas, noted that “supply constraints in the Strait of Hormuz have materialized while tariff transmission continues,” emphasizing that “initial oil price effects will be reflected in March data.”

Goldman economist Manuel Abecasis characterized the present supply disruption as “less alarming than previous instances that generated inflationary pressures,” pointing to its constrained magnitude and scope.

Corporate Results and Geopolitical Developments

Delta Air Lines releases quarterly earnings Wednesday morning before market opening. The carrier’s financial performance will illuminate aviation industry pressures from elevated jet fuel expenses. Constellation Brands and Levi Strauss additionally report during the week.

Financial analysts anticipate S&P 500 earnings expansion exceeding 13% overall, per FactSet data.

Oil prices have escalated beyond 50% since hostilities commenced five weeks earlier. Strait of Hormuz shipping activity remains virtually nonexistent. Trump conducted a Monday briefing alongside military leadership as a self-determined deadline for waterway reopening nears.

Capital.com analyst Daniela Hathorn observed that “financial markets have shifted from anticipating conflict resolution to pricing escalation likelihood.”

Rystad Energy’s chief oil analyst Paola Rodriguez-Masiu indicated that temporary inventory cushions that previously contained price increases are now depleting.

The Federal Reserve’s March policy meeting minutes become available Wednesday at 2 p.m. ET. Market participants broadly anticipate unchanged rates at the upcoming monthly session.