Earnings and Iran Diplomacy Drive Stocks")

Key Takeaways

- Both the S&P 500 and Nasdaq reached fresh all-time highs last week, extending their winning streak to three consecutive weeks

- Tesla delivers Q1 financial results on Wednesday, with focus on the company’s artificial intelligence and robotics initiatives

- Diplomatic progress with Iran regarding the Strait of Hormuz triggered a significant decline in crude oil prices

- The Magnificent Seven tech giants surged 9% across the last five trading sessions

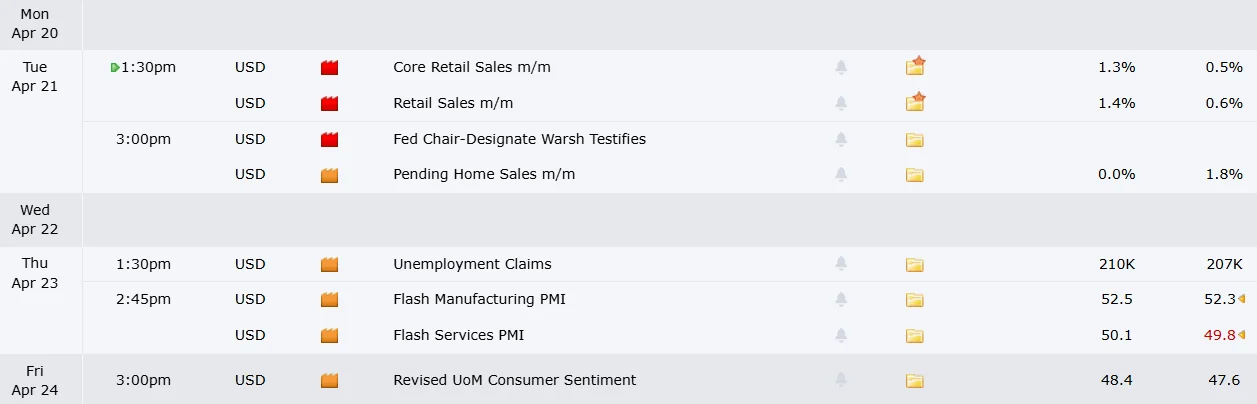

- Tuesday’s March retail sales report will offer critical insights into consumer behavior amid elevated wartime inflation

Equity markets concluded another impressive week with two of the three major benchmarks achieving record territory. The S&P 500 climbed 4.5% over the five-day period, while the Nasdaq advanced 6.8%, and the Dow Jones Industrial Average added 3.2%. This marked the third straight weekly advance for all three indices.

The surge was predominantly fueled by encouraging developments in diplomatic relations between the United States and Iran. Late Friday, Iran’s top diplomat announced the Strait of Hormuz remained “completely open” to commercial shipping operations. President Trump subsequently confirmed Iran had committed to pausing its nuclear enrichment activities and pledged to permanently keep the strategic waterway accessible. Additional negotiations were slated for the weekend.

Crude oil markets responded with sharp declines. Energy analysts at Rystad Energy characterized the diplomatic breakthrough as a “market-moving development of the first order.” However, industry specialists cautioned that market normalization could require weeks or potentially months, even with a finalized agreement. Hundreds of vessels remain stranded in Persian Gulf waters, while Middle Eastern crude production has been slashed by approximately 12.4 million barrels daily.

The Magnificent Seven technology stocks, monitored through a specialized exchange-traded fund, jumped 9% during the five-session period and are nearing their previous peak levels. Taiwan Semiconductor unveiled first-quarter financial results that exceeded analyst projections, posting earnings per share growth of 66% compared to the prior year alongside 40% revenue expansion.

The head of Americas equity strategy at HSBC projected investors should anticipate a “banner Q1 earnings season,” with particular strength expected in technology sectors. The Magnificent Seven group is forecast to deliver 20% earnings expansion, surpassing the 12% growth anticipated for the broader S&P 500.

Tesla Takes Center Stage

Tesla announces first-quarter financial performance on Wednesday. The electric vehicle manufacturer snapped an eight-week decline on Friday. Chief Executive Elon Musk disclosed that Tesla is completing final design work on its AI5 semiconductor, engineered for electric vehicles, training infrastructure, and Optimus robotic systems. Reuters separately indicated Tesla is recruiting chip design specialists in Taiwan.

Tesla has unveiled intentions to manufacture proprietary chips at a production site called Terafab, enlisting Intel as a strategic collaborator. Industry observers note that establishing an internal chip manufacturing capability would represent an enormous engineering undertaking.

UBS equity analyst Joseph Spak observed that the stock “trades more on sentiment, narrative and momentum than fundamentals.” He highlighted risks surrounding electric vehicle market demand, energy supply constraints, and limited advancement on autonomous taxi services and Optimus development, while maintaining Tesla’s leadership position in physical artificial intelligence applications.

Additional Market Catalysts

Intel is scheduled to release quarterly results on Thursday. The semiconductor manufacturer reached its highest intraday valuation since 2000 during Friday’s trading session.

Airline financial reports from Alaska Air, United Airlines, and American Airlines will reveal how carriers are navigating dramatically elevated jet fuel expenses. United Airlines Chief Executive Scott Kirby recently suggested a possible acquisition of American Airlines.

Tuesday delivers March retail sales figures from the Census Bureau. Economic forecasters project a 1.3% monthly increase. The University of Michigan’s consumer sentiment index on Friday will also attract significant attention. Its preliminary April measurement plunged to a historic nadir of 47.6 earlier this month.

UnitedHealth Group announces results on Tuesday, with shares already facing headwinds from reported scrutiny of its insurance billing procedures and an unanticipated executive leadership transition.

Jefferies equity analyst Michael Toomey warned that the technology sector may be “very near the end of this rally,” predicting markets will “consolidate in the near-term.”