Key Takeaways

- Major U.S. equity indexes tumbled last week, leaving the Nasdaq down 10% for 2025

- Oil prices have skyrocketed more than 45% as the Strait of Hormuz crisis continues

- Friday’s March employment report forecast shows modest gains of 50,000–56,000 jobs

- Economic anxiety driven by conflict pushed consumer confidence to December lows

- Market participants now see a 22% probability of Fed rate increases through late 2026

Investors face a compressed trading week dominated by volatile energy markets, deteriorating technical conditions, and crucial employment data that may reshape the Federal Reserve’s policy trajectory.

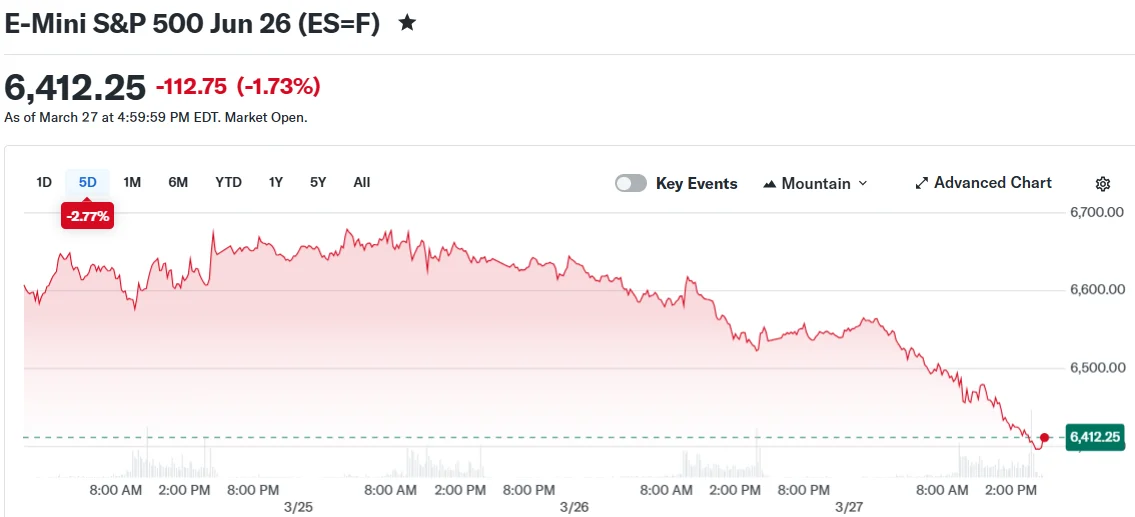

The S&P 500 declined 2.12% over the past five sessions, settling at 6,368.85. The Dow Jones Industrial Average retreated 1.73%, including an approximately 800-point plunge on Friday’s session. The tech-heavy Nasdaq dropped 2.2% Friday and has surrendered roughly 10% year-to-date. Significantly, all three benchmark indexes have breached their 52-week moving averages—a technical development suggesting sustained momentum has deteriorated.

The primary catalyst remains the U.S.-Israeli confrontation with Iran, now extending into its fifth week. The strategic Strait of Hormuz continues its functional closure, eliminating 15 to 16 million barrels daily from international supply chains. Brent crude has appreciated beyond 45%, while WTI crude has climbed over 50% across the previous 30 days.

BP’s chief economist Gareth Ramsay characterized the Strait of Hormuz disruption as “every analyst’s study piece, or worst nightmare that we thought could never happen.” Iranian parliamentary speaker Mohammad Baqer Qalibaf declared the waterway “cannot be the same as before.”

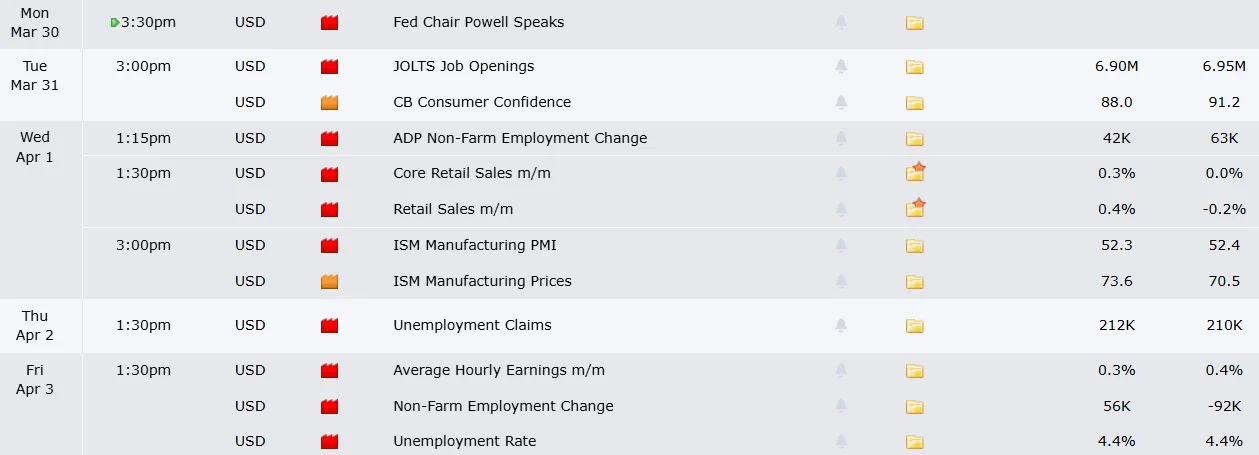

Employment Report Takes Spotlight

Friday’s nonfarm payrolls release represents the week’s most anticipated economic indicator. Analyst consensus anticipates approximately 50,000 to 56,000 March additions, following February’s surprising 92,000-job contraction. The unemployment rate is projected to remain unchanged at 4.4%.

Goldman Sachs economist Pierfrancesco Mei projects elevated energy costs will subtract roughly 10,000 monthly payroll additions through December. BNP Paribas economist Andrew Husby suggested a more pronounced energy disruption would be necessary to disrupt the prevailing pattern of minimal hiring coupled with limited terminations.

Preceding Friday’s headline release, market participants will monitor Tuesday’s consumer confidence metrics, Wednesday’s JOLTS job openings alongside ADP private payroll estimates, and Thursday’s weekly unemployment insurance claims.

Central Bank Policy Outlook Shifts

Fixed-income markets have begun incorporating expectations for a less accommodative Federal Reserve posture. The 10-year Treasury yield advanced to 4.48%, marking its peak since July. Two-year yields climbed to 4%, accumulating over 30 basis points since the central bank’s most recent policy meeting.

BofA Global Research economist Aditya Bhave observed markets seem to be “anticipating a more hawkish Fed reaction function.” Trading activity now reflects a 22% likelihood of a quarter-point rate increase materializing by end-2026.

Headline inflation metrics are projected to approach 3.5% on an annual basis in upcoming months as national gasoline prices approach $4 per gallon.

Regarding corporate developments, Nike delivers quarterly results Tuesday, with particular attention on Chinese market demand trends. ConAgra, Lamb Weston, and Cal-Maine Foods publish results Wednesday. Tesla is scheduled to unveil monthly delivery figures during the week.

Federal Reserve Chair Jerome Powell addresses audiences Monday, with investors scrutinizing commentary for monetary policy direction clues.