TLDR

- Crude markets saw modest gains of approximately 0.3% Thursday as U.S.-Iran diplomatic negotiations commenced in Geneva

- Energy analysts at ING suggest successful negotiations could strip as much as $10 per barrel in geopolitical risk from current pricing

- Commercial crude stockpiles in the United States surged by 16 million barrels, marking the most significant weekly increase since early 2023

- Market observers anticipate OPEC+ will greenlight production increases beginning in April during upcoming weekend meetings

- Improved Kazakh crude flows and declining offshore storage levels indicate strengthening physical market supply

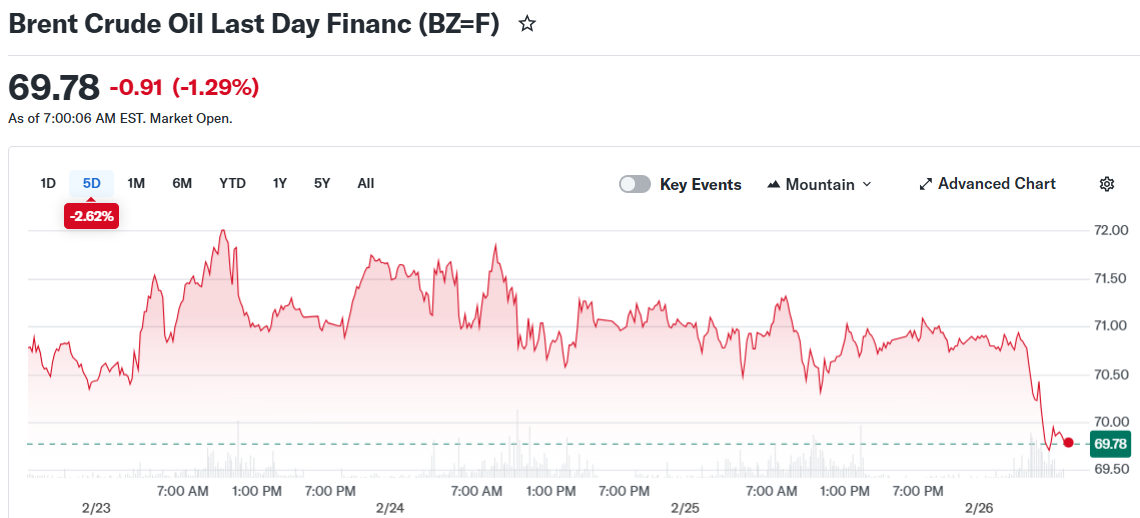

Crude benchmarks posted modest gains Thursday as market participants braced for the third iteration of nuclear discussions between Washington and Tehran. Brent benchmark prices climbed 0.3% to approximately $71 per barrel, with West Texas Intermediate following suit at roughly $65.55.

The diplomatic sessions are taking place in Geneva, where U.S. special envoy Steve Witkoff alongside Jared Kushner are set to engage Iranian counterparts regarding Tehran’s atomic energy ambitions and missile development initiatives.

Iranian Foreign Minister Abbas Araqchi expressed optimism that a diplomatic breakthrough remains achievable provided both parties approach discussions with genuine intent. Meanwhile, President Trump cautioned that unfavorable consequences await should substantive advancement fail to materialize.

Trump established a 10-to-15-day deadline for reaching an agreement and maintained pressure on Iran throughout his State of the Union remarks. Market analysts at Tradu observed that America’s enhanced military presence across the Middle East ensures conflict possibilities remain viable.

As a significant OPEC member, Iran’s production capacity carries substantial market weight. Supply interruptions from Iranian fields or transit disruptions through the strategically critical Strait of Hormuz could trigger considerable price spikes.

Energy analysts at ING project that positive diplomatic outcomes could progressively eliminate up to $10 per barrel in geopolitical risk currently embedded in market valuations. Conversely, negotiation failures would preserve upside risk, though markets may adopt a wait-and-see approach regarding American escalation before fully adjusting.

A Well-Supplied Market Weighs on Prices

From a supply perspective, figures released by the U.S. Energy Information Administration exerted bearish influence. Commercial petroleum reserves expanded by 16 million barrels during the week concluding February 20. This figure substantially exceeded analyst projections and represented the largest single-week accumulation since February 2023.

Motor fuel stockpiles contracted by approximately 1 million barrels across the identical timeframe. Distillate inventories registered a marginal increase of roughly 250,000 barrels, while refining capacity utilization decreased.

Additionally, pricing differentials between immediate delivery and deferred Brent contracts have narrowed. Market participants typically interpret this pattern as evidence of improving physical oil market availability.

Kazakhstan’s crude shipments via the Caspian Pipeline Consortium facility are normalizing following earlier operational challenges. Declining volumes held in floating storage vessels suggest previously embargoed supplies are successfully entering commercial channels, according to industry analysts.

OPEC+ Supply Decision Looms

The OPEC+ coalition is scheduled to convene this weekend. ING’s analytical team predicts the cartel will authorize production increases commencing in April.

Should this materialize concurrent with U.S.-Iran tensions easing, market specialists anticipate deteriorating fundamental conditions would translate into reduced benchmark pricing. The convergence of expanding stockpiles, recovering supply channels, and potential Iranian diplomatic resolution provides multiple catalysts for downward price pressure.

The Geneva diplomatic sessions were set to commence later Thursday, February 26.