Key Takeaways

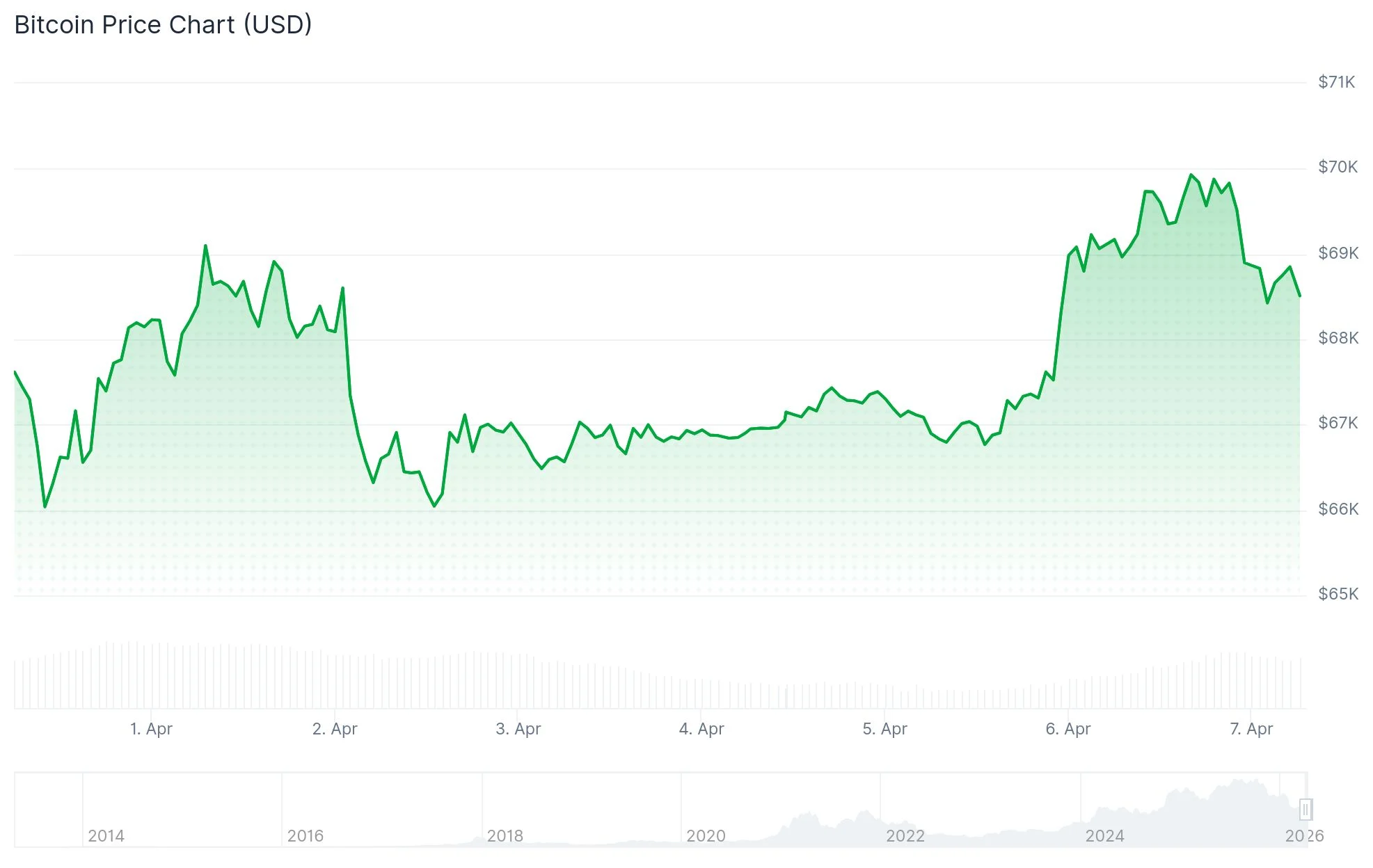

- Bitcoin retreated to $68,589 following a short-lived ceasefire rally, maintaining its six-week trading corridor between $65K and $73K

- A brief Monday surge sparked $196.7 million in liquidations among short sellers before Tehran rejected the proposed ceasefire terms

- President Trump issued a midnight Tuesday ultimatum for Iran to reach an agreement, warning of infrastructure destruction without compliance

- Crude oil prices climbed above $112 per barrel amid mounting geopolitical tensions, with Brent approaching $115.66

- Wall Street futures turned negative Tuesday morning despite modest Monday gains across major indices

Bitcoin declined to $68,589 during Tuesday’s Asian trading session following the evaporation of Monday’s rally momentum. The downturn coincided with President Donald Trump’s establishment of a Tuesday midnight ultimatum for Iran to agree to peace terms or face significant military action.

Monday’s market enthusiasm stemmed from an Axios intelligence report suggesting a potential 45-day cessation of hostilities. This development temporarily lifted Bitcoin above the $69,000 threshold and forced $196.7 million worth of bearish positions to close. However, the bullish momentum sustained for approximately half a day.

Tehran subsequently turned down the ceasefire framework through Pakistani intermediaries. Iranian officials insisted on comprehensive war termination, complete sanctions removal, financial reconstruction assistance, and guaranteed maritime security through the Strait of Hormuz.

Ether decreased 1% to reach $2,104. Solana experienced a 2.7% decline to $79.75. XRP fell 1.6% to $1.32. Dogecoin decreased 2.2% to $0.09. BNB remained largely unchanged at $598.

“This movement appears less related to fundamental changes and more about traders being caught in unfavorable positions,” explained Diana Pires, chief business officer at sFOX. Negative market sentiment had been accumulating prior to the ceasefire news, forcing rapid unwinding of short positions.

Crude Oil Rallies Following Trump’s Forceful Statement

The President warned of destroying “every bridge in Iran” and rendering all power facilities inoperative should negotiations fail by Tuesday midnight. Paradoxically, he simultaneously indicated that discussions were “going well.”

US crude advanced beyond $112 per barrel. Brent traded around $115.66, representing a 2.9% session increase. Escalating oil valuations compound existing macroeconomic uncertainty.

Equity futures weakened Tuesday morning approaching the ultimatum deadline. S&P 500-linked contracts and Nasdaq 100 futures decreased 0.4% and 0.5% respectively. Dow futures retreated approximately 0.2%.

Equity Markets and Economic Indicators Under Scrutiny

Notwithstanding Tuesday’s futures weakness, Monday concluded positively. The S&P 500 registered nearly a 0.5% increase. The Nasdaq achieved comparable advancement. The Dow climbed over 160 points.

Strait of Hormuz shipping traffic intensified this week, offering moderate relief. Chinese and Japanese ports received the highest tanker volumes, alleviating certain supply constraints.

March US services sector data revealed decelerating economic growth. Employment declined at the steepest pace since 2023. Input cost inflation accelerated. These mixed signals provide no definitive guidance for Federal Reserve monetary policy decisions.

Critical inflation metrics arrive Friday. Market participants are simultaneously monitoring preliminary February durable goods orders scheduled for Tuesday morning release. Delta earnings are anticipated Wednesday.

Trump utilized Truth Social to pressure Iran regarding Strait reopening, while separately declaring that “the American people would like to see us come home,” suggesting potential domestic pressure for conflict de-escalation.

Bitcoin has remained confined within the $65,000 to $73,000 trading band throughout the entire conflict period. Trump’s Tuesday midnight deadline will probably dictate which boundary faces immediate testing.